Estate Planning 2026: Navigating New Tax Exemptions

Estate planning in 2026 necessitates a thorough understanding of new federal gift and estate tax exemptions to effectively preserve wealth and minimize potential tax liabilities for beneficiaries.

As 2026 approaches, the landscape of wealth transfer is set for significant changes, making estate planning in 2026 a critical topic for many American families. Understanding the nuances of new federal gift and estate tax exemptions isn’t just about compliance; it’s about strategically safeguarding your legacy and ensuring your assets are distributed according to your wishes, with minimal tax burden. This article will guide you through these anticipated shifts and offer actionable insights for proactive planning.

Understanding the Federal Gift and Estate Tax Landscape

The federal gift and estate tax system in the United States is designed to tax the transfer of wealth from one individual to another, either during life (gifts) or at death (estates). This system has evolved significantly over time, with exemption amounts and tax rates subject to legislative changes. For individuals and families with substantial assets, these taxes can represent a considerable financial impact, making informed planning indispensable.

Historically, the exemption amounts have fluctuated, often driven by economic conditions and political priorities. These exemptions allow a certain amount of wealth to be transferred tax-free. Any amount exceeding this exemption is typically subject to a federal tax rate, which can be as high as 40%. Therefore, staying updated on these figures is paramount for effective wealth management.

Current Exemption Levels and Their Impact

Currently, the federal gift and estate tax exemption, combined with the generation-skipping transfer (GST) tax exemption, is at historically high levels. This has provided a significant window of opportunity for many to transfer wealth without incurring federal transfer taxes. However, this favorable environment is not permanent, and future adjustments are on the horizon.

- High Exemption Amounts: The current exemptions allow for substantial tax-free transfers.

- Unified Credit: The gift and estate tax exemptions are unified, meaning a single credit applies to both lifetime gifts and transfers at death.

- Portability: Spouses can elect to port any unused exemption to the surviving spouse, effectively doubling the exemption for married couples.

These high exemption levels have allowed many high-net-worth individuals to implement sophisticated estate planning strategies that leverage these amounts. However, the anticipated changes in 2026 will require a re-evaluation of these strategies to ensure continued effectiveness and compliance with new regulations. Proactive engagement with financial and legal advisors is highly recommended to adapt to these shifts.

The Sunset of the TCJA Provisions in 2026

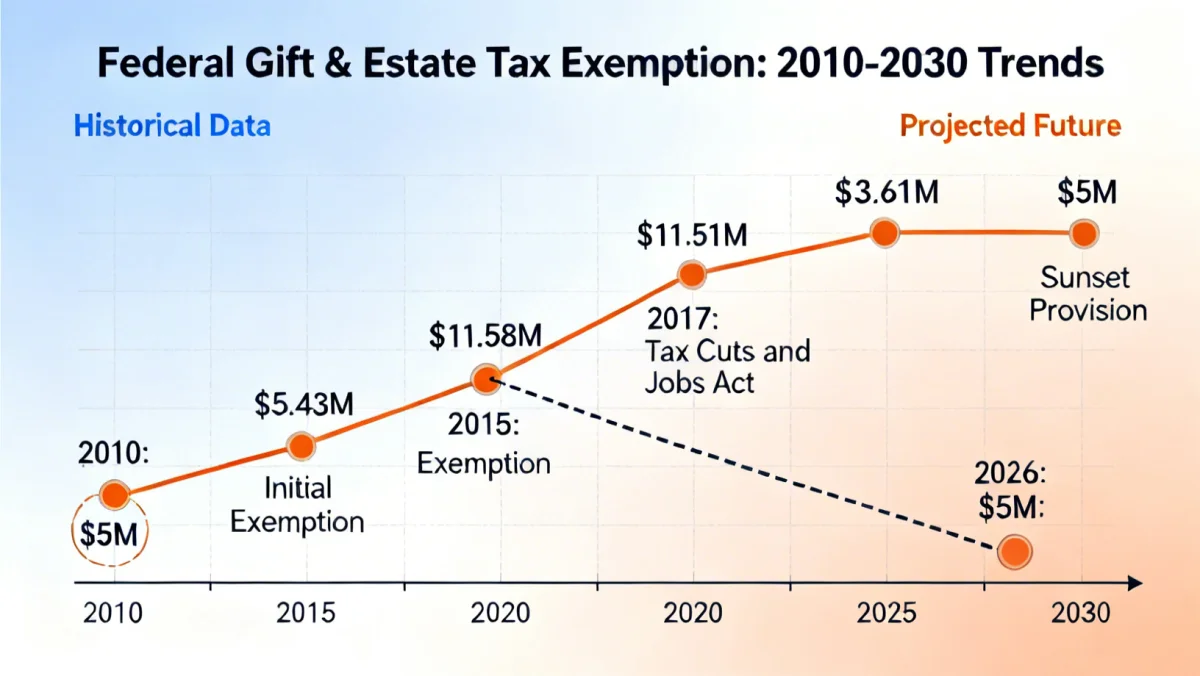

The Tax Cuts and Jobs Act (TCJA) of 2017 significantly increased the federal gift and estate tax exemption amounts. This legislative change provided a temporary, but substantial, increase in the amount of wealth that could be transferred free of federal estate and gift taxes. However, a key aspect of the TCJA was that many of its provisions, including the increased exemption amounts, were set to expire, or ‘sunset,’ at the end of 2025.

This sunset provision means that, absent new legislation, the exemption amounts will revert to their pre-TCJA levels, adjusted for inflation, starting January 1, 2026. This change is poised to have a profound impact on estate planning for many individuals and families, particularly those with estates that currently fall below the exemption threshold but would exceed it under the reduced limits.

Projected Exemption Reductions

While the exact inflation-adjusted figures will only be known closer to 2026, it is widely anticipated that the federal gift and estate tax exemption will be approximately halved. This reduction will significantly decrease the amount of wealth an individual can transfer tax-free, leading to a much larger pool of estates potentially subject to federal estate tax.

For example, if the current exemption is around $13.61 million per individual in 2024, it could fall to roughly $7 million per individual (adjusted for inflation) in 2026. This substantial drop means that many estates that were not previously concerned about federal estate tax will suddenly find themselves within the taxable range. This shift necessitates immediate attention to existing estate plans.

- Significant Reduction: Expect the exemption to be roughly half of its current level.

- Increased Taxable Estates: More estates will become subject to federal estate tax.

- Urgency for Review: Existing plans must be reviewed and potentially revised before 2026.

The impending reduction is not merely a technical adjustment; it represents a fundamental change in how wealth transfer will be taxed. Individuals and families need to proactively engage with their estate planning attorneys and financial advisors to understand the implications for their specific situations and to implement strategies that mitigate potential tax liabilities.

Strategic Estate Planning Before 2026

Given the anticipated reduction in federal gift and estate tax exemptions, the period leading up to 2026 presents a critical window for strategic estate planning. Acting now can help leverage the higher current exemptions and potentially save millions in future estate taxes. This proactive approach involves reviewing current assets, understanding family goals, and implementing appropriate wealth transfer strategies.

Many individuals are considering making substantial gifts before the end of 2025 to utilize the higher exemption amounts. This strategy, often referred to as ‘gifting out the exemption,’ can lock in the current favorable tax treatment. It is essential, however, to ensure that such gifts align with your overall financial goals and do not compromise your financial security.

Leveraging Lifetime Gifting Opportunities

One of the most effective strategies to mitigate the impact of reduced exemptions is to utilize the current high lifetime gift tax exemption. By making gifts to heirs or trusts before 2026, you can remove assets from your taxable estate at today’s higher exemption levels. This not only reduces your potential estate tax liability but also shifts future appreciation of those gifted assets out of your estate.

Consideration should be given to various gifting vehicles, such as irrevocable trusts, which can provide asset protection and control over how the assets are distributed. However, these decisions require careful legal and tax analysis to ensure they meet your specific objectives and comply with all regulations.

- Irrevocable Trusts: A powerful tool for long-term wealth transfer and asset protection.

- Grantor Retained Annuity Trusts (GRATs): Can transfer future appreciation of assets with minimal gift tax consequences.

- Spousal Lifetime Access Trusts (SLATs): Allows one spouse to make gifts into a trust for the benefit of the other spouse, utilizing their exemption while maintaining indirect access to the funds.

Engaging with an experienced estate planning attorney is crucial to determine the most suitable gifting strategies for your situation. They can help navigate the complexities of gift tax rules, ensure proper documentation, and align your gifting plan with your broader estate planning goals. This proactive stance can make a significant difference in preserving your family’s wealth.

Impact on High-Net-Worth Individuals and Families

The impending changes in federal gift and estate tax exemptions will disproportionately affect high-net-worth individuals and families. For those whose estates currently fall comfortably within the high exemption limits, the reduction could push them into a taxable position. This shift necessitates a comprehensive re-evaluation of their existing estate plans and a consideration of advanced strategies.

Many high-net-worth individuals have structured their estates based on the current tax environment, often relying on the large exemptions to avoid federal estate taxes. The sunset of the TCJA provisions means that these plans may no longer be optimal or even effective in achieving their intended goals. Therefore, a thorough review and potential restructuring are imperative.

Advanced Planning Strategies for Larger Estates

For larger estates, the strategies extend beyond simple gifting. These may include more complex trust structures, charitable giving, and business succession planning. The goal is to minimize the taxable estate while ensuring that assets are managed and distributed according to the grantor’s wishes and family needs.

Charitable Remainder Trusts (CRTs) and Charitable Lead Trusts (CLTs) can be powerful tools for individuals with philanthropic goals. These trusts can provide income streams to the grantor or beneficiaries while ultimately benefiting a charity, often resulting in significant estate tax deductions. Business owners may also need to revisit their succession plans to account for potential increases in estate tax liabilities, ensuring the continuity of their enterprises.

Moreover, the use of sophisticated techniques like installment sales to intentionally defective grantor trusts (IDGTs) can be particularly effective. These strategies allow for the sale of appreciating assets to a trust for a promissory note, effectively freezing the value of the asset in the grantor’s estate while transferring future appreciation to the trust beneficiaries outside of the taxable estate. This requires careful execution and professional guidance.

- Irrevocable Life Insurance Trusts (ILITs): Can remove life insurance proceeds from the taxable estate.

- Family Limited Partnerships (FLPs) or Limited Liability Companies (LLCs): Used for transferring assets to younger generations with valuation discounts.

- Qualified Personal Residence Trusts (QPRTs): Allows for gifting a personal residence while retaining the right to live there for a term of years.

The complexity of these strategies underscores the importance of working with a team of experienced professionals, including estate attorneys, tax advisors, and financial planners. Together, they can develop a tailored plan that addresses the specific needs and goals of the high-net-worth family, navigating the intricate tax laws effectively.

The Role of State Estate and Inheritance Taxes

While federal gift and estate tax exemptions are a major concern, it’s crucial not to overlook the impact of state-level estate and inheritance taxes. Several states impose their own estate taxes, inheritance taxes, or both, which can significantly reduce the value of an inheritance, even if an estate falls below the federal exemption threshold. The interplay between federal and state taxes adds another layer of complexity to estate planning.

State estate taxes are typically levied on the total value of the deceased’s estate before it is distributed to heirs, similar to the federal estate tax. Inheritance taxes, on the other hand, are paid by the beneficiaries based on the value of the assets they receive and their relationship to the deceased. The rules, exemption amounts, and tax rates for these state-level taxes vary widely from state to state.

Navigating State-Specific Regulations

For individuals residing in states with their own estate or inheritance taxes, the planning process becomes even more intricate. A plan that is effective for federal tax purposes might not be optimal for state taxes. For instance, some states have much lower estate tax exemptions than the federal level, meaning an estate could be subject to state estate tax even if it avoids federal tax.

Understanding your state’s specific laws is paramount. This might involve considering strategies like changing domicile if feasible, or structuring assets in ways that minimize state tax exposure. For example, some states offer deductions or exemptions for certain types of property or transfers to specific beneficiaries. It’s not uncommon for strategies to be developed that address both federal and state tax implications simultaneously.

- Understand State Exemptions: Be aware of your state’s specific estate or inheritance tax thresholds.

- Consider Domicile: If contemplating a move, research the tax implications of different states.

- State-Specific Trusts: Some states have unique trust laws that can be leveraged for tax planning.

The interaction between federal and state tax laws means that a holistic approach to estate planning is essential. A comprehensive plan should not only address the federal gift and estate tax exemptions but also carefully consider and plan for any applicable state-level taxes to ensure maximum wealth preservation and efficient distribution to heirs. Professional advice tailored to your specific state is indispensable.

Reviewing and Updating Your Estate Plan

The approaching changes in federal gift and estate tax exemptions make 2025 a critical year for reviewing and potentially updating your existing estate plan. Even if you believe your current plan is robust, the shift in tax laws could render some provisions less effective or even counterproductive. A periodic review is always a good practice, but the 2026 sunset provisions create an urgent need for reevaluation.

An outdated estate plan can lead to unintended consequences, including higher tax liabilities, disputes among beneficiaries, or assets not being distributed according to your current wishes. Life events such as marriage, divorce, birth of children or grandchildren, and significant changes in wealth also warrant a review of your plan. The upcoming tax changes simply add another compelling reason to act now.

Key Elements to Re-evaluate

When reviewing your estate plan, several key elements should be scrutinized in light of the 2026 tax law changes:

- Beneficiary Designations: Ensure that beneficiaries on life insurance policies, retirement accounts, and other assets are current and align with your intentions.

- Trusts: Re-evaluate existing trusts to determine if their provisions still align with your goals and the new tax environment. Consider if new trusts, such as irrevocable trusts for gifting, would be beneficial.

- Wills and Powers of Attorney: Confirm that your will accurately reflects your wishes for asset distribution and guardianship, and that your powers of attorney are current and designate appropriate individuals.

- Asset Titling: Review how your assets are titled. Joint ownership, for example, can have different implications for estate taxes and probate depending on the state and asset type.

- Business Succession Plans: If you own a business, ensure your succession plan accounts for potential changes in estate tax liabilities and valuation methods.

Beyond these specific elements, it’s also important to have open and honest discussions with your family about your estate plan. While these conversations can be challenging, they help ensure that your wishes are understood and can prevent future disagreements. A well-communicated plan is often as important as a well-drafted one.

Ultimately, a comprehensive review with your estate planning attorney and financial advisor will help identify any gaps or areas that need adjustment. They can provide guidance on how to best adapt your plan to the new tax landscape, ensuring your legacy is protected and your wishes are honored.

| Key Point | Brief Description |

|---|---|

| 2026 Exemption Sunset | Federal gift and estate tax exemptions will approximately halve, impacting more estates. |

| Lifetime Gifting | Utilize higher current exemptions by making gifts before 2026 to reduce future taxable estate. |

| Advanced Strategies | High-net-worth individuals should consider complex trusts and charitable giving for wealth preservation. |

| State Tax Consideration | Account for state-specific estate and inheritance taxes, as they can significantly impact distributions. |

Frequently Asked Questions About 2026 Estate Planning

In 2026, the federal gift and estate tax exemption amounts are expected to revert to their pre-2018 levels, adjusted for inflation. This means a significant reduction, potentially halving the current exemption, making more estates subject to federal estate tax.

Many advisors suggest considering large gifts before 2026 to leverage the higher current exemption amounts. This can remove assets and their future appreciation from your taxable estate. However, consult with a financial advisor to ensure it aligns with your personal financial security.

Portability of the unused deceased spousal unused exclusion (DSUE) amount will still be available. However, the amount that can be ported will be based on the reduced exemption levels in effect at the time of the second spouse’s death, if after 2025.

State estate and inheritance taxes are crucial. Some states have lower exemption thresholds than the federal government, meaning an estate could be subject to state tax even if it avoids federal tax. Always consider both federal and state laws.

It’s highly advisable to review and potentially update your estate plan well before the end of 2025. This allows ample time to implement strategies that leverage the current higher exemptions and prepare for the anticipated changes in 2026.

Conclusion

The impending changes to federal gift and estate tax exemptions in 2026 mark a pivotal moment for estate planning. The sunset of the TCJA provisions will significantly reduce the amount of wealth that can be transferred tax-free, impacting a broader range of estates. Proactive engagement with these shifts, through strategic lifetime gifting, careful review of existing plans, and consideration of advanced wealth transfer techniques, is not merely recommended but essential. By understanding the evolving landscape and working with qualified professionals, individuals and families can effectively navigate these changes, protect their legacies, and ensure their assets are distributed according to their wishes, minimizing potential tax burdens for future generations.