Maximize 2026 Student Loan Repayment: 4 Key Strategies

Effectively managing student loan debt in 2026 involves understanding and implementing key strategies such as income-driven repayment plans, strategic refinancing, exploring forgiveness programs, and optimizing payment approaches to achieve financial stability.

Navigating student loan repayment can feel like a daunting task, especially as economic landscapes and policy changes continue to evolve. For those facing their financial obligations in the coming year, understanding how to maximize your 2026 student loan repayment options: 4 strategies is not just beneficial, it’s essential. This guide will help you decipher the complexities, empowering you to make informed decisions that safeguard your financial future.

Understanding Income-Driven Repayment (IDR) Plans in 2026

Income-Driven Repayment (IDR) plans have long been a lifeline for borrowers struggling with high monthly student loan payments relative to their income. In 2026, these plans continue to offer crucial flexibility, adjusting your monthly payment based on your discretionary income and family size. It’s vital to stay updated on any modifications to these programs, as they can significantly impact your financial burden.

These plans are designed to prevent default and provide a more manageable path to loan repayment. By enrolling in an IDR plan, your monthly payment can be as low as $0, depending on your income. This can free up funds for other essential expenses or savings, offering a critical buffer during financially challenging times.

The Evolving Landscape of IDR Plans

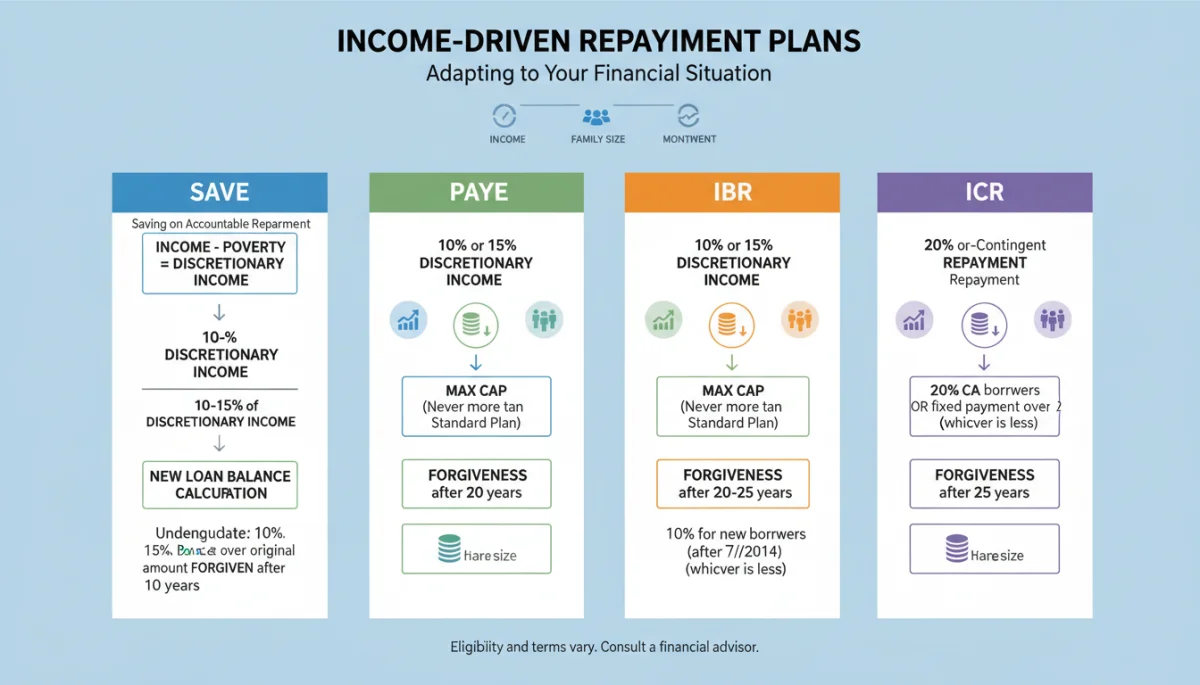

The federal government periodically reviews and updates its IDR programs. Staying informed about these changes is paramount for maximizing your benefits. The SAVE Plan (Saving on a Valuable Education), for instance, has introduced significant improvements for many borrowers, potentially lowering payments and preventing interest capitalization.

- SAVE Plan (Saving on a Valuable Education): Offers the lowest monthly payments among IDR plans for most borrowers, calculated based on a larger percentage of discretionary income definition.

- PAYE (Pay As You Earn): Caps payments at 10% of discretionary income, and offers forgiveness after 20 years of payments.

- IBR (Income-Based Repayment): Payments are generally 10% or 15% of discretionary income, with forgiveness after 20 or 25 years.

- ICR (Income-Contingent Repayment): The oldest IDR plan, payments are either 20% of discretionary income or what you’d pay on a fixed 12-year plan, whichever is less.

Each IDR plan has its own set of rules regarding eligibility, payment calculation, and the duration until any remaining balance is forgiven. Choosing the right plan requires a careful assessment of your current financial situation, your loan types, and your long-term financial goals. Consulting with a financial advisor specializing in student loans can provide personalized guidance.

The annual recertification process for IDR plans is another key aspect borrowers must manage. Failing to recertify on time can lead to your payments reverting to the standard plan, potentially causing a significant increase and capitalized interest. Always mark your calendar and submit your updated income and family size information promptly to ensure your payments remain affordable.

Evaluating Refinancing Opportunities in 2026

Refinancing student loans can be a powerful strategy to reduce your interest rate, lower your monthly payments, or even shorten your repayment term. However, it’s a decision that requires careful consideration, as it involves replacing federal loans with private ones, which means giving up federal protections.

The refinancing market in 2026 will likely continue to be competitive, with various private lenders offering attractive rates. It’s crucial to shop around and compare offers to find the best terms for your specific financial profile. A lower interest rate can save you thousands of dollars over the life of your loan.

Key Considerations Before Refinancing

Before making the leap to refinance, take stock of your current loans and your financial health. Refinancing is generally most beneficial for borrowers with a strong credit score, a stable income, and a clear understanding of the trade-offs involved. Federal loan benefits, such as access to IDR plans, deferment, forbearance, and potential forgiveness programs, are lost once you refinance into a private loan.

- Interest Rates: Compare fixed vs. variable rates. Fixed rates offer predictability, while variable rates may start lower but can fluctuate.

- Loan Terms: Shorter terms mean higher monthly payments but less interest paid overall. Longer terms reduce monthly payments but increase total interest.

- Credit Score: A higher credit score typically qualifies you for better interest rates. Consider improving your credit before applying.

- Co-signer Options: If your credit isn’t strong enough, a co-signer with excellent credit can help you secure a better rate.

Refinancing can be particularly advantageous if you have private student loans with high interest rates, as these loans typically lack the federal protections you’d be giving up. For federal loans, the decision is more nuanced. Weigh the potential interest savings against the loss of federal benefits carefully. Some borrowers choose to refinance only a portion of their federal loans, keeping others federal to retain some protections.

The application process for refinancing usually involves submitting financial documentation, including income verification and credit history. Lenders will assess your ability to repay the new loan. Be prepared to provide accurate and complete information to streamline the process and increase your chances of approval for the best possible terms.

Exploring Loan Forgiveness and Discharge Programs

Beyond standard repayment and refinancing, several programs offer the possibility of loan forgiveness or discharge, significantly reducing or eliminating your student loan debt. These programs are often tied to specific professions, public service, or certain life circumstances. Understanding the eligibility requirements for these options is crucial for anyone seeking to maximize their 2026 student loan repayment options.

The landscape of forgiveness programs can be complex, with varying criteria and application processes. It’s essential to research and identify which programs you might qualify for, as they can provide immense financial relief. Many programs require a certain number of qualifying payments or years of service.

Public Service Loan Forgiveness (PSLF) and Other Avenues

The Public Service Loan Forgiveness (PSLF) program remains a cornerstone for individuals working in eligible public service jobs. After making 120 qualifying monthly payments under a qualifying repayment plan while working full-time for a qualifying employer, your remaining federal student loan balance may be forgiven. This program has seen significant attention and some temporary waivers in recent years, making it an even more attractive option.

- Public Service Loan Forgiveness (PSLF): Forgives the remaining balance on Direct Loans after 120 qualifying payments while working full-time for a U.S. federal, state, local, or tribal government or not-for-profit organization.

- Teacher Loan Forgiveness: Offers up to $17,500 in forgiveness for eligible teachers who have taught full-time for five complete and consecutive academic years in low-income schools or educational service agencies.

- Perkins Loan Cancellation: Available to borrowers in certain professions, such as teaching, nursing, or law enforcement, with a percentage of the loan canceled for each year of service.

- Total and Permanent Disability (TPD) Discharge: Allows for the discharge of federal student loans if you are totally and permanently disabled.

- Borrower Defense to Repayment: Provides a path to loan discharge if your school misled you or engaged in other misconduct.

It’s important to note that only federal Direct Loans are eligible for PSLF. If you have Federal Family Education Loan (FFEL) Program loans or Perkins Loans, you may need to consolidate them into a Direct Consolidation Loan to become eligible. Always confirm your loan types and employment eligibility to ensure you are on the correct path for PSLF.

Beyond PSLF, various state-specific loan repayment assistance programs (LRAPs) exist for professionals in high-need areas, such as healthcare and law. These programs offer additional avenues for reducing your debt burden. Researching opportunities available in your state or profession can uncover valuable benefits.

Optimizing Payment Strategies and Financial Literacy

Beyond choosing the right repayment plan or pursuing forgiveness, optimizing your payment strategies and enhancing your financial literacy are crucial for long-term success in managing student loan debt. Small, consistent efforts can lead to significant savings and a faster path to debt freedom. This involves understanding your budget, making extra payments when possible, and staying disciplined.

Developing a solid financial plan that incorporates your student loan payments is key. This plan should not only cover your loan obligations but also address your savings goals, emergency fund, and other financial aspirations. Financial literacy empowers you to make proactive decisions rather than reactive ones.

Smart Payment Approaches for 2026

Even if you’re on an IDR plan or pursuing forgiveness, there are ways to accelerate your repayment or make it more efficient. Understanding how interest accrues and how payments are applied can help you devise a strategy that works best for your situation. Small, consistent overpayments can dramatically reduce the total interest paid.

- Paying More Than the Minimum: Even an extra $50 or $100 per month can significantly reduce your total interest and repayment time.

- Bi-weekly Payments: By making half of your monthly payment every two weeks, you effectively make an extra payment each year, shortening your loan term.

- Targeting High-Interest Loans: If you have multiple loans, focus extra payments on the one with the highest interest rate first (the “debt avalanche” method).

- Automate Payments: Setting up automatic payments ensures you never miss a due date and may even qualify you for a small interest rate discount from some servicers.

Another often-overlooked strategy is to allocate any windfalls, such as tax refunds, bonuses, or unexpected gifts, towards your student loans. Even a one-time lump sum payment can make a noticeable difference in the overall cost and duration of your loan. Make sure to instruct your servicer to apply these extra payments to the principal balance, rather than advancing your due date.

Regularly reviewing your financial situation and making adjustments to your repayment strategy is also important. Life circumstances change, and your student loan plan should adapt accordingly. Stay engaged with your loan servicer, ask questions, and utilize the resources they provide to ensure you’re always on the most advantageous path.

Navigating Tax Implications of Student Loan Repayment

Understanding the tax implications associated with student loan repayment and potential forgiveness is a critical, yet often overlooked, aspect of maximizing your strategies for 2026. Certain payments or forgiven amounts can have either tax benefits or liabilities that significantly impact your overall financial picture. Being aware of these can help you plan effectively and avoid unexpected tax burdens.

The U.S. tax code offers several provisions related to student loans, such as deductions for student loan interest paid. However, it also treats some types of loan forgiveness as taxable income, which can be a surprise for borrowers expecting complete financial relief. Proactive planning and consultation with a tax professional are highly recommended.

Student Loan Interest Deduction and Forgiveness Taxation

The student loan interest deduction allows eligible taxpayers to deduct the amount of student loan interest paid during the year, up to a certain limit. This deduction can reduce your taxable income, potentially lowering your overall tax liability. It’s an important benefit for many borrowers, especially those making substantial interest payments.

- Student Loan Interest Deduction: You can deduct the amount of interest you paid on a qualified student loan, up to $2,500, from your taxable income.

- Taxable Forgiveness: Generally, forgiven student loan debt is considered taxable income by the IRS, with some key exceptions.

- PSLF Exception: Debt forgiven under the Public Service Loan Forgiveness program is explicitly non-taxable at the federal level.

- Temporary Federal Exemption: Previously, certain federal student loan forgiveness was temporarily excluded from federal taxable income through 2025. Be aware of its status for 2026.

For individuals whose loans are forgiven through income-driven repayment plans after 20 or 25 years, the forgiven amount typically counts as taxable income. This can result in a significant tax bill in the year the debt is forgiven. It’s crucial to plan for this potential tax liability by saving in advance or exploring other tax mitigation strategies.

The tax treatment of student loan forgiveness can also vary by state. While federal law might exempt certain types of forgiveness from federal income tax, your state might still consider it taxable. Therefore, it’s essential to check your state’s tax laws or consult with a local tax advisor to understand the full implications for your personal situation.

Leveraging Resources and Professional Guidance

Successfully navigating your student loan repayment journey in 2026 doesn’t mean you have to go it alone. A wealth of resources and professional guidance is available to help you understand your options, make informed decisions, and stay on track. Leveraging these tools can provide clarity, confidence, and ultimately, better financial outcomes.

From government websites to non-profit organizations and certified financial planners, various entities are dedicated to assisting borrowers. Knowing where to turn for accurate and reliable information is a crucial step in maximizing your repayment strategies.

Where to Find Reliable Support and Information

The U.S. Department of Education’s Federal Student Aid (FSA) website is the authoritative source for information on federal student loans. It provides details on all federal repayment plans, forgiveness programs, and important updates. Your loan servicer is also a primary point of contact for questions specific to your loans.

- Federal Student Aid (FSA) Website: Your go-to source for official information on federal student loans, repayment plans, and forgiveness programs.

- Loan Servicer: Contact your loan servicer directly for specific details about your loans, payment history, and enrollment in plans.

- Non-profit Credit Counseling Agencies: These organizations often offer free or low-cost advice on debt management, including student loans.

- Certified Financial Planners (CFPs): For complex financial situations or comprehensive planning, a CFP can provide personalized advice.

- Online Calculators and Tools: Many websites offer calculators to compare repayment plans, estimate forgiveness amounts, and project interest savings.

When seeking professional advice, ensure that the individuals or organizations you consult are reputable and qualified. Be wary of companies that charge high fees for services you can access for free through your loan servicer or the FSA website. A legitimate advisor will focus on educating you about your options rather than pushing you into specific products.

Regularly checking your loan status and payment history through your servicer’s online portal is also a good practice. This helps you monitor your progress, identify any discrepancies, and ensure you’re on track with your chosen repayment strategy. Proactive engagement with your loans is a hallmark of effective financial management.

Preparing for Future Policy Changes and Economic Shifts

The student loan landscape is dynamic, influenced by economic conditions, legislative actions, and administrative policies. As you plan your 2026 student loan repayment options, it’s prudent to anticipate and prepare for potential future changes. Staying informed and building financial resilience can help you adapt to any shifts without derailing your progress.

Economic shifts, such as changes in interest rates or job market fluctuations, can directly impact your ability to make payments or the attractiveness of refinancing. Policy changes, whether legislative or executive, can alter the terms of existing programs or introduce new ones. Being prepared for these eventualities is a key component of a robust repayment strategy.

Strategies for Adaptability and Resilience

One of the most effective ways to prepare for future uncertainties is to build a strong financial foundation. This includes establishing an emergency fund, minimizing other high-interest debt, and maintaining a healthy credit score. These measures provide a buffer against unexpected financial challenges and enhance your flexibility.

- Build an Emergency Fund: Having 3-6 months of living expenses saved can provide a critical safety net if your income changes.

- Monitor Policy Developments: Stay updated on news from the Department of Education, Congress, and financial news outlets regarding student loan policy.

- Maintain Financial Flexibility: Avoid over-committing to rigid financial plans that don’t allow for adjustments based on changing circumstances.

- Review Your Strategy Annually: Revisit your repayment plan and overall financial situation at least once a year to ensure it still aligns with your goals and current conditions.

Engaging with reliable news sources and official government communications is essential for staying informed about potential policy changes. Subscribing to email updates from Federal Student Aid or following reputable financial journalists can keep you abreast of developments that might affect your loans.

Furthermore, consider scenario planning. What would happen if interest rates rise? How would a job loss impact your ability to pay? By thinking through these possibilities, you can develop contingency plans and adjust your current strategies to be more resilient. This proactive approach ensures that you are not caught off guard by unforeseen circumstances, allowing you to maintain control over your student loan repayment journey.

| Key Strategy | Brief Description |

|---|---|

| Income-Driven Plans | Adjust monthly payments based on income and family size; vital for affordability. |

| Refinancing | Potentially lower interest rates or monthly payments by switching to a private loan. |

| Loan Forgiveness | Programs like PSLF or Teacher Forgiveness can eliminate remaining debt. |

| Payment Optimization | Making extra payments or using bi-weekly schedules to reduce total interest. |

Frequently Asked Questions About 2026 Student Loan Repayment

The SAVE Plan is an income-driven repayment plan that often results in the lowest monthly payments for many federal student loan borrowers. It calculates payments based on a larger percentage of your discretionary income and prevents interest capitalization, potentially offering significant relief in 2026.

Refinancing a federal student loan into a private loan can offer lower interest rates, but it means losing federal protections like income-driven repayment, deferment, and forgiveness programs. It’s best suited for borrowers with stable income and excellent credit who are confident they won’t need federal benefits.

To qualify for PSLF in 2026, you must have Direct Loans, work full-time for an eligible government or non-profit organization, and make 120 qualifying monthly payments under an income-driven repayment plan. Consolidating other federal loans into Direct Loans may be necessary.

Generally, most forgiven student loan debt is considered taxable income by the IRS, with the notable exception of Public Service Loan Forgiveness (PSLF). It’s crucial to consult a tax professional to understand the specific tax implications for your situation in 2026, as state laws may also vary.

To pay off student loans faster, consider making extra payments, utilizing a bi-weekly payment schedule, or targeting high-interest loans first. Automating payments can also help ensure consistency and may even provide a small interest rate discount from some loan servicers, accelerating your debt freedom.

Conclusion

Successfully managing your student loan debt in 2026 requires a proactive and informed approach. By delving into the intricacies of income-driven repayment plans, carefully evaluating refinancing opportunities, exploring various loan forgiveness programs, and adopting optimized payment strategies, borrowers can significantly improve their financial outlook. Staying informed about policy changes and leveraging available resources are also critical steps toward achieving financial stability and ultimately, student loan freedom. Taking control of your repayment journey today can pave the way for a more secure financial future.