2026 Social Security Benefits Adjustments: Essential Guide

The 2026 Social Security benefits adjustments are critical for current and future beneficiaries, encompassing cost-of-living allowances, earnings limits, and potential legislative changes that will impact financial planning and retirement income across the United States.

Are you wondering how the upcoming changes will impact your financial future? Understanding the 2026 Social Security Benefits Adjustments: What You Need to Know is paramount for anyone relying on or planning for Social Security. These adjustments can significantly influence retirement planning and overall financial well-being, making it essential to stay informed and prepare proactively.

Understanding the Cost-of-Living Adjustment (COLA)

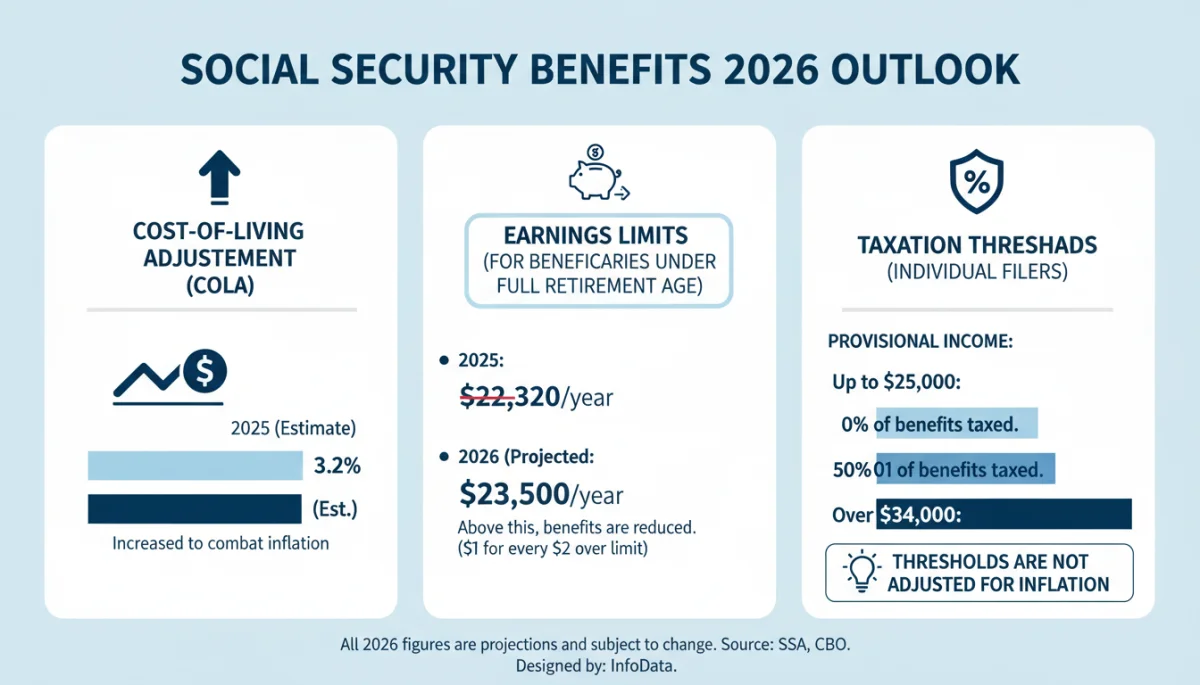

The Cost-of-Living Adjustment, or COLA, is a crucial element of Social Security benefits. Each year, COLA aims to ensure that the purchasing power of Social Security benefits doesn’t erode due to inflation. For 2026, the COLA calculation will be based on specific economic indicators, directly impacting the monthly payments received by millions of Americans.

The Social Security Administration (SSA) typically announces the COLA in October, based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). This index measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. A higher CPI-W generally translates to a larger COLA, providing beneficiaries with increased payments to keep pace with rising costs.

How COLA is Calculated

The calculation of COLA is a precise process that involves comparing the average CPI-W for the third quarter of the current year (July, August, and September) with the average CPI-W for the third quarter of the last year in which a COLA was payable. The percentage increase between these two averages determines the COLA percentage. This method ensures that the adjustment reflects recent inflationary trends, maintaining the real value of benefits.

- CPI-W Index: The primary metric used to determine the annual COLA.

- Comparison Period: Third-quarter CPI-W data is crucial for the calculation.

- Protection Against Inflation: COLA’s main purpose is to prevent the erosion of purchasing power.

It’s important to remember that while COLA helps protect against inflation, it doesn’t always perfectly align with every individual’s personal spending habits. However, it remains the most significant mechanism for adjusting benefits annually. Beneficiaries should monitor economic forecasts leading up to the announcement to get an early sense of potential changes.

Changes to Maximum Taxable Earnings in 2026

Another significant adjustment for 2026 involves the maximum amount of earnings subject to Social Security taxes. This figure, often referred to as the ‘taxable maximum’ or ‘wage base,’ is critical for both current workers and future beneficiaries. It dictates how much of an individual’s income is subject to Social Security payroll taxes and also sets the cap for how much earnings can be credited toward future benefits.

Historically, the taxable maximum increases each year based on the national average wage index. As wages rise across the country, so does the amount of income subject to Social Security taxes. This adjustment ensures the long-term solvency of the Social Security program by capturing a proportional share of growing wages. Higher earners will see more of their income taxed, which directly contributes to the trust funds.

Impact on High-Income Earners

For individuals whose earnings exceed the current taxable maximum, an increase in this limit means a larger portion of their income will be subject to Social Security taxes. This directly affects their take-home pay. Conversely, for those earning below the new limit, there will be no change in the percentage of income taxed, though their overall tax liability might still be affected by other factors.

- Increased Taxable Income: More earnings become subject to Social Security taxes.

- Benefit Calculation: Higher taxed income can lead to higher future benefits, up to a certain point.

- Payroll Deductions: Workers earning above the previous limit will see increased Social Security withholdings.

Understanding these changes is vital for financial planning, especially for those in higher income brackets. It can influence budgeting, investment strategies, and retirement savings goals. Employers also need to be aware of these adjustments for payroll processing and tax compliance.

Adjustments to Social Security Earnings Limits

For beneficiaries who continue to work while receiving Social Security benefits, earnings limits are a critical consideration. These limits determine how much you can earn before your benefits are temporarily reduced. For 2026, these earnings limits are also expected to undergo adjustments, impacting how much working retirees can keep from their benefits.

The Social Security Administration has different earnings limits depending on whether you are below your full retirement age (FRA) or will reach your FRA during the year. Once you reach your FRA, earnings limits no longer apply, and you can earn any amount without your benefits being reduced. These limits are adjusted annually to reflect changes in the national average wage index.

How Earnings Limits Affect Benefits

If you are below your FRA for the entire year, the SSA will deduct $1 from your benefits for every $2 you earn above the annual limit. For those who reach their FRA during the year, the reduction is less severe: $1 is deducted for every $3 earned above a different, higher limit, but only earnings before the month you reach FRA are counted. These rules are designed to balance work incentives with the purpose of Social Security as a retirement safety net.

- Below FRA: Stricter earnings limits apply, leading to benefit reductions.

- Year of FRA: A higher limit applies, and only earnings before FRA are counted.

- At or Above FRA: No earnings limits; benefits are not reduced regardless of income.

It is crucial for individuals close to retirement or already receiving benefits to understand these limits. Exceeding them without proper planning can lead to unexpected reductions in Social Security payments. Consulting with a financial advisor or the SSA directly can help navigate these complexities and optimize your benefit strategy.

Potential Legislative Changes and Their Impact

Beyond the automatic annual adjustments, Social Security is often a subject of legislative debate. For 2026, there may be discussions or proposals for more fundamental reforms to ensure the program’s long-term solvency. These potential legislative changes could have significant and far-reaching impacts on current and future beneficiaries, altering aspects beyond just the COLA or earnings limits.

Discussions often revolve around various proposals, such as increasing the full retirement age, adjusting the formula for calculating benefits, or changing the tax structure that funds Social Security. While these are often contentious topics, the need to address the program’s financial outlook keeps them on the legislative agenda. Any significant changes would likely be phased in over time to minimize disruption.

Areas of Potential Reform

Lawmakers might consider a range of options, each with its own set of implications. For example, an increase in the full retirement age would mean individuals would have to work longer to receive their full benefits or accept reduced benefits if they claim earlier. Changes to the benefit formula, such as adjusting the indexation method, could alter the amount of benefits future retirees receive.

- Full Retirement Age: Potential increases could affect claiming strategies.

- Benefit Calculation: Modifications to formulas might alter future payment amounts.

- Taxation: Changes to the Social Security tax rate or the taxable maximum could be considered.

Staying informed about these potential legislative developments is essential. Public engagement and awareness can also play a role in shaping these policy discussions. Beneficiaries and future retirees should pay close attention to news from Congress and advocacy groups regarding Social Security reform.

Medicare Premium Deductions and Social Security

For many Social Security beneficiaries, Medicare premiums are automatically deducted from their monthly payments. The relationship between these two programs means that changes in Medicare Part B premiums can directly affect the net Social Security benefit received. For 2026, adjustments to Medicare premiums are expected, which will influence the final amount beneficiaries see in their bank accounts.

Medicare Part B covers medically necessary services and preventive services. The standard premium for Part B changes annually, often increasing due to rising healthcare costs. These premium increases can sometimes offset a portion of the COLA increase, meaning the effective increase in net Social Security benefits might be less than the announced COLA percentage. This dynamic is particularly important for budgeting.

Income-Related Monthly Adjustment Amounts (IRMAA)

Higher-income beneficiaries also face Income-Related Monthly Adjustment Amounts (IRMAA) for Medicare Part B and Part D. These surcharges mean that individuals with incomes above certain thresholds pay higher premiums. For 2026, these income thresholds are also subject to adjustment, which could pull more beneficiaries into higher premium tiers or shift existing ones. This makes understanding your income’s impact crucial.

- Part B Premiums: Automatically deducted from most Social Security payments.

- COLA Offset: Medicare premium increases can reduce the net effect of COLA.

- IRMAA Thresholds: Higher earners face additional surcharges based on income.

It is vital for beneficiaries to review their annual Medicare premium statements and compare them with their Social Security benefit statements. This helps in accurately forecasting their net income and planning their finances accordingly. Understanding the interplay between Social Security and Medicare is a key component of comprehensive retirement financial planning.

Planning for Your 2026 Social Security Benefits

Proactive planning is essential to maximize your Social Security benefits and ensure financial stability in retirement. Given the various adjustments expected in 2026, taking steps now to understand and prepare for these changes can make a significant difference. This includes reviewing your earnings record, understanding claiming strategies, and considering how other income sources interact with your benefits.

Start by accessing your Social Security statement online through the SSA website. This statement provides a personalized estimate of your future benefits based on your earnings history. Reviewing it regularly helps identify any discrepancies and allows you to project your income more accurately. Understanding your projected benefits is the first step in effective retirement planning.

Optimizing Your Claiming Strategy

Choosing when to claim Social Security benefits is one of the most critical decisions you will make. You can start receiving benefits as early as age 62, but your monthly payment will be permanently reduced. Waiting until your full retirement age or even until age 70 can significantly increase your monthly benefit amount. The optimal claiming strategy depends on various factors, including your health, other retirement savings, and spousal benefits.

- Review Your Statement: Regularly check your Social Security earnings record for accuracy.

- Claiming Age: Understand how claiming early or late impacts your monthly benefit.

- Financial Advisor: Consider consulting a professional for personalized guidance.

Considering all these factors will lead to a more informed decision regarding your Social Security benefits. The adjustments in 2026 serve as a reminder that these programs are dynamic, and staying updated is crucial for sound financial management throughout your retirement years.

Navigating Future Social Security Challenges

While the annual adjustments for 2026 are important, it’s also crucial to consider the broader, long-term challenges facing the Social Security program. The program’s financial outlook is a recurring topic, with projections indicating that the trust funds may be unable to pay 100% of scheduled benefits in the distant future without legislative action. Understanding these challenges can help individuals plan more robustly for their retirement.

Demographic shifts, such as increasing life expectancies and declining birth rates, contribute significantly to these long-term concerns. Fewer workers are contributing per beneficiary, putting pressure on the system. These trends underscore the importance of not relying solely on Social Security for retirement income and diversifying savings strategies.

Diversifying Retirement Income

Building a diversified retirement income portfolio is a prudent strategy given the uncertainties surrounding Social Security’s long-term future. This includes maximizing contributions to 401(k)s, IRAs, and other investment vehicles. Personal savings, pensions, and other assets can provide a crucial buffer and complement your Social Security benefits, ensuring a more secure retirement.

- Long-Term Solvency: Be aware of the trust fund projections and potential future reforms.

- Demographic Trends: Understand how population changes impact the program.

- Personal Savings: Supplement Social Security with 401(k)s, IRAs, and other investments.

By staying informed about both the annual adjustments and the long-term outlook, individuals can make more strategic decisions. Planning for a future where Social Security may provide a foundational, but not exclusive, source of retirement income is a wise approach. This comprehensive view helps in creating a resilient financial plan for the years to come.

| Key Point | Brief Description |

|---|---|

| COLA Impact | Ensures benefits keep pace with inflation, announced in October 2025 for 2026. |

| Taxable Maximum | The earnings limit subject to Social Security taxes is expected to increase. |

| Earnings Limits | Rules for working beneficiaries below Full Retirement Age will be adjusted. |

| Medicare Premiums | Changes to Part B premiums may affect net Social Security benefit amounts. |

Frequently Asked Questions About 2026 Social Security Adjustments

The official Cost-of-Living Adjustment (COLA) for 2026 is typically announced by the Social Security Administration (SSA) in October of 2025. This announcement is based on inflation data from the third quarter (July, August, and September) of the preceding year.

The maximum amount of earnings subject to Social Security taxes, known as the taxable maximum, is adjusted annually based on the national average wage index. For 2026, it is expected to increase, meaning higher earners will pay Social Security taxes on a larger portion of their income.

No, once you reach your full retirement age (FRA), Social Security earnings limits no longer apply. You can earn any amount of income without your benefits being reduced. Earnings limits only affect beneficiaries who are working while receiving benefits before reaching their FRA.

Medicare Part B premiums are typically deducted directly from your monthly Social Security benefit. Therefore, any increase in Medicare premiums can reduce the net amount you receive from Social Security, even if there’s a COLA increase.

While annual adjustments are automatic, legislative changes to Social Security are always possible. Discussions often occur regarding the program’s long-term solvency, which could lead to proposals affecting the full retirement age, benefit formulas, or taxation. However, no specific legislative changes are confirmed for 2026 at this time.

Conclusion

The 2026 Social Security Benefits Adjustments are more than mere numbers; they represent critical shifts that will directly influence the financial security of millions of Americans. From the anticipated Cost-of-Living Adjustment (COLA) designed to combat inflation to changes in the maximum taxable earnings and earnings limits for working beneficiaries, each modification requires careful attention. Furthermore, the interplay with Medicare premiums and the ongoing legislative discussions about the program’s long-term future underscore the need for proactive engagement and informed planning. By understanding these adjustments and preparing accordingly, individuals can better ensure their financial well-being and make strategic decisions for a more secure retirement.