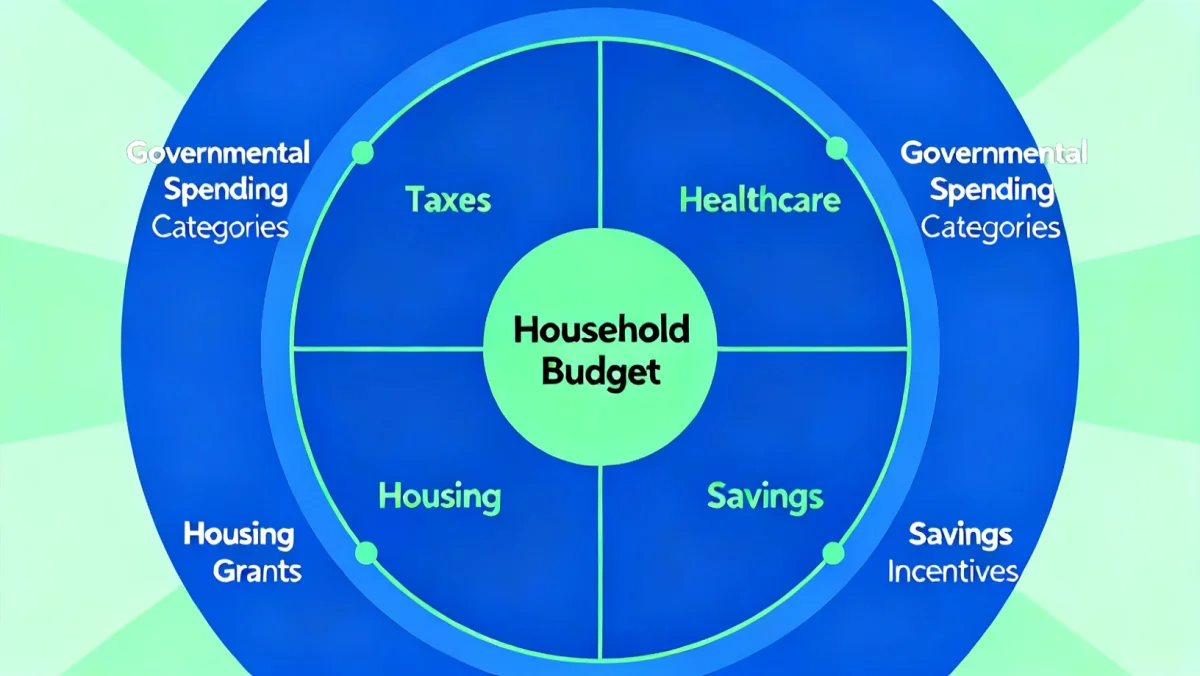

Federal Budget Impact on Personal Finances in 2026

The Federal Budget Impact on personal finances in 2026 will be significant, influencing taxation, healthcare costs, Social Security benefits, and housing affordability, requiring proactive financial planning.

As 2026 approaches, understanding the potential impact of the Federal Budget Impact on Personal Finances in 2026: 4 Key Areas to Monitor becomes crucial for every American household. The decisions made in Washington ripple through our daily lives, affecting everything from our paychecks to our retirement plans. Being informed is the first step toward safeguarding your financial future.

Understanding the Federal Budget Landscape in 2026

The federal budget is more than just a collection of numbers; it’s a strategic document that outlines the government’s priorities and how it plans to fund them. For 2026, several factors are shaping this landscape, including ongoing economic shifts, evolving social programs, and geopolitical considerations. These elements collectively dictate the fiscal environment that will directly or indirectly affect every individual’s financial standing.

Analyzing the budget requires looking beyond headline figures. It involves delving into specific allocations for various departments and programs, understanding projected revenues, and recognizing potential deficits or surpluses. Each of these components plays a vital role in determining where adjustments might be made, and consequently, where the impact on personal finances will be felt most acutely. The interplay of these complex factors creates a dynamic and often unpredictable financial outlook.

Key Economic Indicators and Their Influence

Several economic indicators are particularly influential in shaping the federal budget. Inflation rates, GDP growth, and unemployment figures directly affect government revenue through taxes and spending on social safety nets. For instance, higher inflation can erode the purchasing power of fixed incomes, prompting calls for increased social benefits, which in turn pressures the budget.

- Inflation Trends: Prolonged inflation can lead to higher costs for government programs and potentially higher interest rates on federal debt.

- GDP Growth Projections: Robust economic growth typically translates to increased tax revenues, providing more flexibility for budget allocations.

- Unemployment Rates: High unemployment often necessitates increased government spending on unemployment benefits and other support programs.

Political Climate and Budgetary Priorities

The political climate significantly influences budgetary decisions. Different administrations and legislative majorities often prioritize distinct areas, such as defense, healthcare, education, or infrastructure. These priorities can shift rapidly, leading to substantial changes in funding for various sectors. Understanding the current political leanings helps anticipate where budget cuts or increases might occur.

Furthermore, bipartisan agreements or stalemates can delay or alter budget proposals, creating uncertainty. This political dance directly impacts the stability and predictability of federal spending, which can have downstream effects on state budgets and, ultimately, individual financial planning. Staying abreast of legislative developments is therefore essential for anticipating financial shifts.

In summary, the federal budget for 2026 is a multifaceted construct influenced by economic realities and political intentions. These foundational elements lay the groundwork for how financial implications will manifest across various sectors, directly touching the personal finances of citizens. A comprehensive understanding of this framework is the first step in preparing for the year ahead.

Taxation: Navigating Potential Changes to Your Income and Investments

Taxation is arguably the most direct way the federal budget impacts personal finances. In 2026, we could see significant adjustments to tax codes, affecting everything from individual income tax rates to capital gains and estate taxes. These changes are often driven by the need to fund new initiatives, reduce the national debt, or stimulate economic growth.

Staying informed about proposed tax legislation is crucial. Even minor adjustments to tax brackets, deductions, or credits can have a substantial effect on your take-home pay and investment returns. Proactive financial planning, including consulting with a tax professional, can help you adapt to these changes and optimize your tax strategy.

Income Tax Rate Adjustments

One of the most anticipated areas of change involves individual income tax rates. Depending on the prevailing political climate and economic conditions, there could be shifts in tax brackets, new surcharges for high earners, or even adjustments to standard deductions and personal exemptions. These modifications directly influence how much of your earned income you retain each year.

- Bracket Changes: A shift in income tax brackets could push more individuals into higher or lower tax rates.

- Deduction Limitations: New caps or eliminations of certain deductions could increase taxable income for many.

- Credit Modifications: Changes to tax credits, such as the Child Tax Credit or earned income credits, would affect families and low-income individuals.

Capital Gains and Investment Taxation

Investors should pay close attention to potential changes in capital gains taxes. These taxes apply to profits from the sale of assets like stocks, bonds, and real estate. Any increase in these rates could significantly reduce the net returns on investments, influencing decisions about portfolio management and asset allocation.

Beyond capital gains, other investment-related taxes, such as those on dividends or interest income, might also see adjustments. These changes could prompt investors to reconsider their investment strategies, favoring tax-advantaged accounts or instruments that align better with the new tax landscape. Understanding these nuances is key to preserving investment growth.

Estate and Gift Tax Considerations

For those engaged in estate planning, changes to estate and gift taxes are particularly relevant. The federal government sets thresholds for tax-free transfers of wealth, and these figures can be adjusted. Alterations to these limits or the tax rates applied to transfers above these limits can significantly impact wealth transfer strategies and intergenerational planning.

These tax changes are not merely about compliance; they are about strategic financial management. Understanding the potential shifts in tax policy allows individuals and families to make informed decisions that can protect their wealth, reduce their tax burden, and ensure their financial plans remain robust in a changing environment.

Healthcare Costs: Navigating Subsidies, Premiums, and Program Funding

Healthcare is another critical area where the federal budget directly impacts personal finances. In 2026, potential changes to healthcare subsidies, insurance premiums, and the funding of major programs like Medicare and Medicaid could profoundly affect access to care and out-of-pocket expenses for millions of Americans.

The federal government plays a substantial role in regulating and funding the healthcare sector. Budgetary decisions in this area can influence the availability of affordable health insurance, the scope of covered services, and the financial burden placed on individuals and families. Monitoring these developments is essential for managing your healthcare expenditures effectively.

Impact on Health Insurance Premiums and Subsidies

Government subsidies for health insurance, particularly those offered through the Affordable Care Act (ACA) marketplaces, are subject to budgetary review. Any reduction in these subsidies could lead to higher out-of-pocket premium costs for individuals and families who rely on them to make health insurance affordable. Conversely, increased funding could expand access to more affordable plans.

Changes in federal mandates or regulations could also influence the types of plans available and their associated costs. For example, relaxed regulations might lead to cheaper, less comprehensive plans, while stricter requirements could increase the cost of more robust coverage. These dynamics directly affect how much you pay for your health insurance.

Medicare and Medicaid Funding Outlook

Medicare and Medicaid, two cornerstone federal healthcare programs, are constantly under budgetary scrutiny. Decisions regarding their funding levels for 2026 could impact eligibility requirements, the range of services covered, and the financial contributions required from beneficiaries. For seniors and low-income families, these changes are incredibly significant.

Financial adjustments to these programs might include increased deductibles, co-payments, or limitations on certain medical services. Such changes would shift more of the financial responsibility onto patients, potentially leading to higher personal healthcare expenses. Conversely, enhanced funding could expand benefits or reduce out-of-pocket costs.

Prescription Drug Costs and Innovation

The federal budget also influences prescription drug costs, often through negotiations with pharmaceutical companies or funding for drug research and development. Policies aimed at controlling drug prices, such as allowing Medicare to negotiate drug costs, could lead to significant savings for consumers. However, reduced funding for innovation could also impact the availability of new treatments.

Understanding these potential shifts in healthcare policy and funding is paramount. It allows individuals to anticipate changes in their insurance coverage, plan for potential increases in out-of-pocket costs, and make informed decisions about their healthcare choices. Proactive engagement with healthcare planning can mitigate unexpected financial burdens.

Social Security and Retirement: Securing Your Future Benefits

For millions of Americans, Social Security represents a vital component of their retirement income. The federal budget’s decisions regarding Social Security and other retirement programs in 2026 will be closely watched, as they can determine the stability and adequacy of future benefits. These programs face ongoing challenges related to demographics and funding, making budgetary adjustments a persistent concern.

The long-term solvency of Social Security is a recurring topic in budget discussions. Any legislative changes, however minor, can have profound effects on current and future retirees. Understanding these potential shifts is crucial for effective retirement planning and ensuring your financial security in later life.

Potential Adjustments to Social Security Benefits

One of the most significant areas of concern is the potential for adjustments to Social Security benefits. These could include changes to the full retirement age, modifications to the cost-of-living adjustment (COLA) formula, or alterations to the taxation of benefits. Any of these could directly impact the monthly income retirees receive.

- Full Retirement Age: Increasing the age at which full benefits are received would delay access to full payments for many.

- COLA Formula: A change in the COLA calculation could result in lower annual benefit increases, reducing purchasing power over time.

- Benefit Taxation: Adjustments to the income thresholds at which Social Security benefits become taxable could increase the tax burden for some retirees.

Funding for Retirement Savings Programs

Beyond Social Security, the federal budget can also influence other retirement savings programs. This includes potential changes to the contribution limits for 401(k)s, IRAs, and other tax-advantaged retirement accounts. Such modifications can affect individuals’ ability to save for retirement efficiently and benefit from tax deferrals or exemptions.

Legislative efforts to encourage or discourage certain types of retirement savings could also emerge. For example, new incentives for long-term care insurance or changes to required minimum distributions (RMDs) could alter how individuals manage their retirement assets. These factors necessitate a flexible and informed approach to retirement planning.

Long-Term Solvency and Policy Debates

The ongoing debate about Social Security’s long-term solvency is a central theme in federal budget discussions. Various proposals, such as increasing the payroll tax rate, raising the taxable earnings cap, or adjusting benefits, are frequently discussed. While these are often contentious, their potential implementation would have significant financial implications for workers and retirees.

Monitoring these policy debates and understanding their potential outcomes is essential for anyone relying on Social Security for retirement income. Proactive financial planning, including diversifying retirement savings and seeking professional advice, can help mitigate risks associated with potential changes to these vital programs.

Housing and Infrastructure: Affordability and Local Economic Impact

The federal budget also plays a significant, though often indirect, role in housing affordability and local economic development. Investments in infrastructure, housing programs, and community development initiatives can influence housing costs, job markets, and the overall economic health of regions across the country. These impacts can vary widely depending on specific allocations.

Federal funding for infrastructure projects, such as roads, bridges, and public transit, can stimulate local economies, create jobs, and increase property values in affected areas. Conversely, a lack of investment can lead to stagnation. Understanding these budgetary priorities is key to anticipating regional economic shifts and their impact on personal finances.

Federal Housing Programs and Affordability

Various federal programs aim to address housing affordability, including rental assistance, homeownership initiatives, and support for affordable housing development. Budgetary decisions in 2026 could alter the funding levels for these programs, affecting the availability of assistance for low-income families and first-time homebuyers.

- Rental Assistance: Reduced funding could lead to longer waiting lists or fewer eligible recipients for housing vouchers.

- Homeownership Programs: Changes to FHA loans or down payment assistance programs could impact access to homeownership.

- Affordable Housing Development: Cuts to grants for affordable housing projects could slow the creation of new units, exacerbating housing shortages.

Infrastructure Spending and Local Economies

Significant federal investment in infrastructure can have a cascading effect on local economies. Projects like new transportation networks, improved utilities, and broadband expansion can attract businesses, create employment opportunities, and boost local property values. This can lead to increased economic activity and potentially higher wages in affected regions.

However, a reduction in infrastructure spending could slow economic growth in some areas, potentially impacting job markets and overall financial stability for residents. The types of projects prioritized also matter; investments in green infrastructure, for example, could create new industries and jobs in specific sectors, influencing regional economic landscapes.

Community Development and Urban Planning

Federal funding for community development block grants and other urban planning initiatives also influences local living conditions and economic opportunities. These funds support a wide array of projects, from revitalizing urban centers to improving public services in rural areas. Changes in these allocations can impact the quality of life and economic prospects of communities.

The federal budget’s influence on housing and infrastructure is a long-term play, but its effects are deeply felt at the local level. Understanding these trends allows individuals to make informed decisions about where to live, work, and invest, aligning their personal financial goals with broader economic developments.

Strategies for Personal Financial Resilience in 2026

Given the potential for significant shifts in the federal budget and its subsequent impact on personal finances in 2026, developing a robust strategy for financial resilience is more important than ever. This involves proactive planning, diversified financial approaches, and continuous monitoring of policy changes. Adapting to the evolving landscape can help mitigate risks and capitalize on new opportunities.

Financial resilience isn’t just about weathering storms; it’s about building a foundation that can absorb shocks and pivot effectively when conditions change. This requires a holistic view of your finances, encompassing income, expenses, savings, investments, and debt management, all while staying attuned to external economic and political influences.

Diversifying Income Streams and Savings

Relying on a single source of income can be precarious, especially in an unpredictable economic climate. Exploring additional income streams, such as freelance work, side hustles, or passive investments, can provide a buffer against potential job market fluctuations or changes in wage growth. Diversifying income enhances your financial stability.

- Side Gigs: Engaging in part-time work or consulting can supplement your primary income.

- Investment Income: Building a diversified investment portfolio can provide passive income through dividends or interest.

- Skill Development: Investing in new skills can open doors to higher-paying opportunities or new career paths.

Equally important is building a robust emergency fund. Aim for at least three to six months’ worth of living expenses in an easily accessible savings account. This fund acts as a critical safety net, allowing you to cover unexpected costs or periods of reduced income without resorting to high-interest debt.

Proactive Debt Management and Budgeting

Effective debt management is fundamental to financial resilience. High-interest debt, such as credit card balances, can quickly erode your financial stability, especially if interest rates rise due to federal monetary policy. Prioritizing the reduction of such debt frees up cash flow and reduces financial stress.

A detailed and flexible budget is another indispensable tool. Regularly reviewing your income and expenses allows you to identify areas for potential savings and adjust spending habits as needed. This adaptability is key when facing changes in taxation, healthcare costs, or other budget-related impacts. Automation of savings and bill payments can further streamline this process.

Seeking Professional Financial Guidance

Navigating the complexities of federal budget changes and their personal financial implications can be challenging. Consulting with a qualified financial advisor can provide invaluable insights and personalized strategies. A professional can help you understand the nuances of tax law, optimize investment portfolios, and plan for retirement in a way that accounts for evolving policies.

Regularly reviewing your financial plan with an expert ensures that it remains aligned with your goals and responsive to external shifts. This proactive approach to financial planning is a cornerstone of building long-term resilience and achieving financial security in an ever-changing economic environment.

Anticipating and Adapting to Policy Shifts

The federal budget is a living document, subject to continuous review and adjustment. For 2026, individuals and families must remain vigilant, anticipating policy shifts and adapting their financial strategies accordingly. This involves staying informed about legislative debates, understanding the implications of proposed changes, and being prepared to pivot when necessary.

Adaptability is a key trait of financially resilient individuals. The ability to modify spending habits, adjust investment strategies, or re-evaluate retirement plans in response to new government policies can significantly reduce financial stress and enhance long-term security. A proactive mindset, rather than a reactive one, is essential in this dynamic environment.

Monitoring Legislative Developments

Keeping an eye on legislative developments in Congress and the White House is crucial. Official government websites, reputable financial news outlets, and non-partisan policy analysis organizations can provide reliable information on proposed budget changes and their potential impacts. Subscribing to newsletters or alerts from these sources can help you stay informed.

Understanding the political landscape and the priorities of elected officials can also offer clues about likely policy directions. While predicting the future is impossible, recognizing trends and potential areas of focus allows for more informed anticipation of changes that could affect your finances.

Scenario Planning for Financial Outcomes

Engaging in scenario planning can be a powerful tool for preparing for uncertainty. Consider different potential outcomes of federal budget decisions – for example, what if taxes increase significantly, or if healthcare subsidies are reduced? By modeling these scenarios, you can assess their impact on your personal budget and identify areas where you might need to make adjustments.

This exercise isn’t about predicting the exact future, but rather about preparing for a range of possibilities. It helps you develop contingency plans and build flexibility into your financial strategy, ensuring that you are not caught off guard by unexpected policy shifts. This foresight contributes significantly to overall financial resilience.

Leveraging Financial Tools and Resources

A wealth of financial tools and resources are available to help individuals navigate complex economic environments. Budgeting apps, retirement calculators, investment analysis platforms, and tax planning software can all assist in managing your finances more effectively. Many of these tools offer features that allow you to model different financial scenarios based on potential policy changes.

Furthermore, educational resources from financial institutions, non-profit organizations, and government agencies can enhance your financial literacy. The more you understand about economic principles and policy impacts, the better equipped you will be to make informed decisions and adapt your financial strategy to the evolving federal budget landscape in 2026.

| Key Area | Potential Impact on Personal Finances |

|---|---|

| Taxation | Changes in income tax rates, capital gains, and deductions could affect take-home pay and investment returns. |

| Healthcare Costs | Adjustments to subsidies, premiums, and program funding (Medicare/Medicaid) may alter out-of-pocket expenses. |

| Social Security | Potential modifications to benefits, retirement age, or taxation could influence future retirement income. |

| Housing & Infrastructure | Federal investments or cuts could impact housing affordability, local job markets, and property values. |

Frequently Asked Questions About Federal Budget Impact

Federal tax changes in 2026 could impact your take-home pay through adjustments to income tax brackets, standard deductions, or new tax credits. Higher tax rates or reduced deductions would likely decrease your net income, while favorable changes could increase it. Staying informed on specific legislative updates is key to understanding the direct effect.

The main risks to Social Security benefits from the 2026 federal budget include potential adjustments to the full retirement age, modifications to the cost-of-living adjustment (COLA) formula, or changes in how benefits are taxed. These measures are often discussed to address the program’s long-term solvency, directly impacting future retirees’ income.

Federal healthcare budget decisions can influence your insurance premiums by altering subsidies available through marketplaces, or by changing funding for Medicare and Medicaid. Reductions in subsidies could lead to higher out-of-pocket premium costs, while increased funding or regulatory changes might make insurance more affordable or affect covered services.

Yes, federal infrastructure spending in 2026 can significantly affect your local housing market. Investments in transportation, utilities, or community development can boost local economies, create jobs, and increase property values. Conversely, a lack of investment might lead to slower growth, potentially impacting housing demand and affordability in your area.

To prepare for federal budget changes, you should diversify income streams, build a robust emergency fund, and manage debt proactively. Regularly review your budget and consult with a financial advisor to optimize your tax strategy and investment portfolio. Staying informed about legislative developments will also help you adapt your financial plans effectively.

Conclusion

The Federal Budget Impact on Personal Finances in 2026: 4 Key Areas to Monitor underscores the critical need for proactive financial planning. From taxation and healthcare costs to Social Security and housing, the ripple effects of federal decisions will touch every aspect of a household’s economic well-being. By staying informed, diversifying financial strategies, and seeking professional guidance, individuals can navigate these changes with greater confidence and resilience, safeguarding their financial future in an ever-evolving economic landscape.